Published on April 29, 2025 by Erangi Perera and Oshadi Hettiarachchi

Introduction

Syndicated loans play a significant role in the global financial system, providing access to corporations and governments to large-scale funding for projects and corporate expansions that are too substantial to be managed by a single lender. The syndicated loan market has seen significant growth, expanding from USD1.06tn[1] in 2023 to USD1.2tn in 2024, at a growth rate of 13.2% y/y due to economic growth, corporate mergers and acquisitions, prevailing credit market conditions and global trade dynamics. The market comprises key industry segments such as financial services, energy and power, high technology, industrials, consumer products and services, relies heavily on syndicated loan operations to manage its complexity, with advance loan management system vital to support its rapid evolution.

The increase in syndicated lending has put significant pressure on commercial lending divisions, disclosing major operating deficiencies in lending operations processes. Although banks invest in their overall operations, key issues in syndicated loan operations receive only surface-level attention, leading to heavy manual workloads for back-office divisions. Neglecting to re-think and investing in an advance loan management system of this crucial business segment would not only adversely impact operational efficiency and customer satisfaction but also diminish potential profitability. Syndicated lending is inherently complicated, having to communicate with multiple stakeholders, with some deals involving 100-300 lenders. This complexity is further heightened by the various amendments and restructuring requested by borrowers that require lender approval and voting, diverse repayment schedules and repricing events that enable borrowers to negotiate lower rates in favourable market conditions. The recent transition from LIBOR to local reference rates has contributed to this complexity.

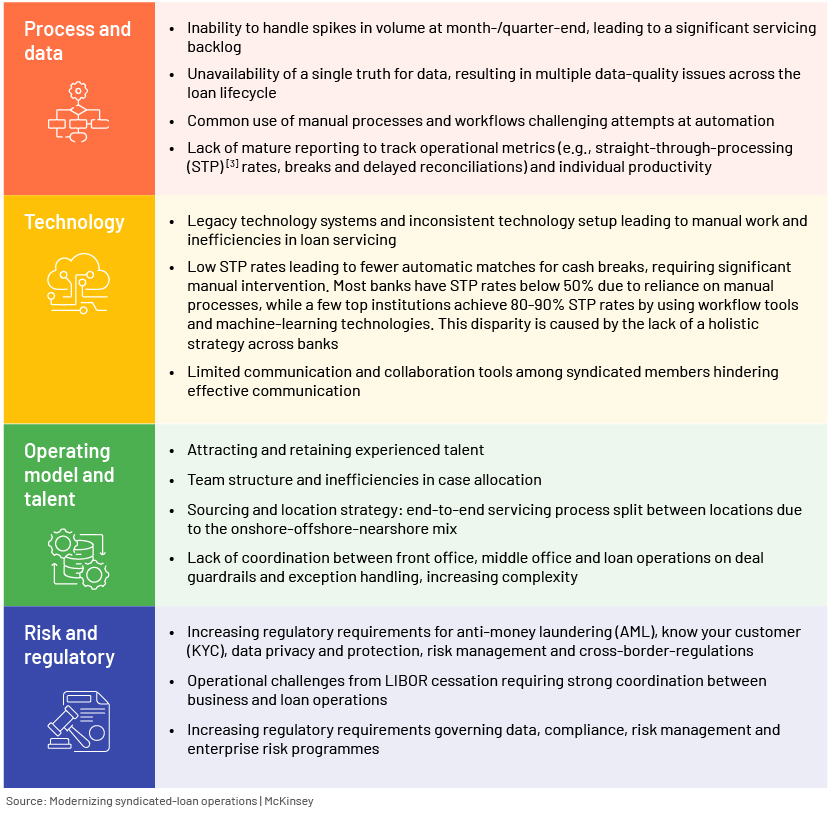

Challenges in syndicated loan operations across banks’ core capabilities

There is still significant reliance on emails, face-to-face meetings and phone calls in confirming deals, according to the front-office teams of many banks.[2].Therefore, maintaining the status quo could limit a bank’s ability to respond to market demands. As syndicated deal volumes and the number of participants increase, syndicated loan operations experience multi-faceted challenges, divided into four main domains, as tabulated below.

Modernising syndicated loan operations with advanced loan management systems

To address these obstacles, banks must strategically rethink and optimise their syndicated loan operations procedure by investing in modern lending solutions with advanced features and capabilities. These advance loan management system would help them reduce manual workloads by overcoming operational deficiencies and enhancing productivity.

Banks are increasingly turning to sophisticated advance loan management system and related technologies to navigate the complexities of syndicated loan operations. These advanced systems, such as Loan IQ, Wall Street Office (WSO), AFS Vision and FIS Commercial Lending Suite, automate tasks, ensure compliance and enhance data accuracy, significantly reducing risks and operating costs. Other systems such as ClearPAR, DebtDomain, Intralinks and Loan Recon support different aspects of syndicated loan operations, from post-trade workflows to secure document sharing and automated reconciliation. These tools are essential for managing large, complex multi-lender deals, tracking cashflow and providing flexible support to small and medium-size business customers.

One of the key features of advanced loan management system is that they support the entire loan lifecycle of a syndicated loan, ensuring end-to-end deal administration from origination to settlement, without or with minimum manual intervention. These systems also minimise the risk of regulatory breaches by ensuring regulatory compliance with built-in controls. Another key feature is ensuring data accuracy and integrity through real-time data management capabilities that ensure all key stakeholders have access to timely information. These systems are also equipped with advanced reconciliation tools to minimise discrepancies and enhance data integrity. Workflow optimisation, advanced collateral management capabilities and rich trading functions that enable muti-branch and multi-currency settlements are some of the other essential features of loan management systems. These advanced features individually and collectively enable banks to achieve a high degree of operating efficiency while maintaining regulatory compliance as required by the industry.

What prevents banks from implementing advanced loan management systems?

Although increasing transaction volumes, driven by significant growth in the syndicated loan market, require that banks modernise loan operations processes by adopting a more strategic and holistic view, banks are often reluctant to do so due to the practical hurdles faced during implementation. One key obstacle identified is incompatibility between advanced loan management system and banks’ legacy platforms that may be outdated. Therefore, the integration process is burdened with another layer of complexity, in addition to the inherent complications of digitalising syndicated loans support. Data validation and migration processes may also become challenging due to potential risks of corruption and loss of data, making them more time-consuming and resource-intensive.

Another key challenge banks face is the substantial effort required to attract and retain knowledge of newly implemented advance loan management system, due to high staff attrition. Studies[4] show that a number of banks faced attrition of 20-70% among onshore, US-centric loan operations staff, causing significant loss of institutional knowledge. Recruiting new staff and constant training complicate the implementation process.

Banks and other financial institutions are expected to adhere to increased and ever-changing regulatory requirements, increasing the difficulty of implementation. In addition to complying with AML and KYC requirements, they need to ensure rigorous borrower and syndicate member verification and transaction monitoring. Furthermore, syndicated loan operations require managing compliance with a number of regulatory frameworks, as they often cross multiple jurisdictions. Global data privacy laws such as Europe’s General Data Protection Regulation designed to maintain high data protection standards also play a crucial role. The Equal Credit Opportunity Act (ECOA), T+1 Settlement Cycle, Basel III and Federal Financial Management Improvement Act (FFMIA) are some of the other key regulations that banks need to consider. To comply with these regulations, they must continue to monitor and update advance loan management systems, another challenge in implementation.

These challenges make implementing an advanced loan management system a substantial undertaking. Access to specialised support and domain expertise would be a game changer, helping banks fully use the benefits of advanced loan management technologies.

How Acuity Knowledge Partners can help

-

Domain expertise. We provide customised solutions to suit the complex requirements demanded by syndicated loan servicing processes, leveraging our experience and expertise in syndicated loan operations and our deep understanding of the banking and finance sector.

-

Integration support. We provide assistance in integrating advanced loan management platforms such as LoanIQ with legacy systems, ensuring minimal disruption and an elevated level of compatibility. This includes reviewing loan agreements, collateral documentation and pricing details and repayment schedules for data verification purposes.

-

Data migration and validation support. We assist in managing end-to-end data migration processes with a high level of accuracy and integrity. This includes data validation support to prevent data loss and corruption.

-

Training and knowledge retention. We conduct comprehensive training programmes to ensure bank staff are fully trained in using the newly implemented advance loan management system. This includes compiling detailed process manuals to address staff attrition and knowledge-retention issues.

-

Regulatory compliance. We ensure that all the systems, processes and manuals are consistent with applicable regulatory guidelines and are updated regularly.

-

Executing loan servicing functions on a client’s existing systems or loan management platforms. This includes deal modification and reconstruction, managing roll-overs, managing queries raised by clients and performing general ledger and month-end report reconciliations. It also includes managing complicated syndicated loan repayment schedules, coordinating with lenders and monitoring disbursements.

Sources:

1. Syndication loans and systems used: A Comprehensive Guide to Syndicated Loans and Bank Debt – Gage Gorman

market-insights_transformation-syndicated-lending.pdf

Comprehensive Guide to Syndicated Loans and Bank Debt: Advanced Insights – Gage Gorman

Syndicated Loans Market Report 2024 – Syndicated Loans Market Size And Share

market-insights_transformation-syndicated-lending.pdf

Syndicated Loan Industry Statistics 2025 • CoinLaw

2. Modernising syndicated loans: Modernizing syndicated-loan operations | McKinsey

market-insights_transformation-syndicated-lending.pdf

3. Loan IQ: Loan IQ: The world's preeminent corporate lending solution

4. Loan syndication support to a global bank | Acuity Knowledge Partners

Lending operations outsourcing | Acuity Knowledge Partners

Loan servicing support to a bank headquartered in France (US book) | Acuity Knowledge Partners

[1] Syndicated Loan Industry Statistics 2025 • CoinLaw

[2] Source: market-insights_transformation-syndicated-lending.pdf

[3] The straight-through processing (STP) rate measures the efficiency of automated financial transaction processing, indicating the percentage of transactions completed electronically without manual intervention.

[4] Source: Modernizing syndicated-loan operations | McKinsey

What's your view?

Thank you for sharing your Comments

Share this on

About the Authors

Erangi Perera has 18 years of professional experience, including 15 years in banking, focusing on loan operations, corporate banking, and accounting. She has hands on experience in platform migration, process improvement, and lean management. Erangi is a Fellow member of CIMA(UK) and holds an MBA, and a BBA from the University of Colombo.

Oshadi Hettiarachchi has 1.5 years of experience in commercial lending. She has been with Acuity Knowledge Partners (Acuity) since Nov-2023. She’s an ACCA affiliate with B.Sc in Business Administration in University of Sri Jayewardenepura.

Blog

Blog

Introduction to the ESG Data Convergence Initiat....

The ESG Data Convergence Initiative (EDCI) is a partnership of private-markets investors t....Read More

Blog

Blog

Advancing portfolio-monitoring tools through tec....

Private equity (PE) and venture capital (VC) firms often face high-pressure, time-sensitiv....Read More

Blog

Blog

Is the US heading towards a hard landing?....

President Trump took back the White House in November 2024, pledging to address inflation ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox